LUMAX Industries | Q1FY20

August 09, 2019

LUMAX Industries

BUY

Y/E March (` cr)

1QFY20

1QFY19

% yoy 4QFY19

% qoq

BUY

Net sales

402

482

(17)

433

(7)

CMP

`1,290

EBITDA

38

41

(5)

31

25

EBITDA margin (%)

9.5

8.4

112bp

7.1

242bp

Target Price

`1,669

PAT

17

20

(17)

14

16

Investment Period

12 Months

For 1QFY2020, Lumax Industries Ltd. (LIL) registered ~17% de-growth on yoy basis

Stock Info

on the consolidated revenue front to `402cr as compared to `482cr. Operating

Sector

Auto-Ancillary

margin improved by 112bps to 9.5%. On the bottom-line front, the company has

Market Cap (` cr)

1,206

Beta

1.3

reported de-growth of ~17% due to poor sales performance.

52 Week High / Low

2,266/912

Avg. Daily Volume

3,865

Slowdown in automobile industry drags the overall volume growth: Lumax registered

Face Value (`)

10

~17% de-growth on yoy basis on the consolidated revenue front to `402cr as

BSE Sensex

37,655

Nifty

11,133

compared to `482cr yoy. The decline in revenue was majorly due to slowdown in

Reuters Code

LUMA.BO

Bloomberg Code

LUMX IN

PVs and production cut announced by OEMs. Going forward, management expects

company to see recovery in sales due to declining interest rate, pick-up in rural

Shareholding Pattern (%)

volume, and pre-buying for BSVI. The company has also added new customers,

Promoters

75.0

Morris Garage (MG Motors) and TVS motors, which are expected to add `45cr in

MF / Banks / Indian Fls

1.1

incremental revenue in FY20.

FII / NRIs / OCBs

0.0

Overall lower sales impacts profitability: Operating margin improved by 112bps to

Indian Public / Others

23.9

9.5% mainly owing to in-house electronic facilities for manufacturing of PCBs, cost

reduction initiatives, and softening commodity prices. On the bottom-line front, the

Abs.(%)

3m

1yr

3yr

company has reported de-growth of ~17% due to poor sales performance.

Sensex

(1.2)

(1.5)

32.4

Outlook and Valuation: Near term outlook looks tough for the industry, however

LUMAXIND

(28.2)

(28.2)

57.2

considering the long term perspective, LIL is a good bet to play on auto growth and

increasing LED penetration, which will help Lumax to grow above the industry rate

going forward. Thus, we main our buy recommendation on the stock with target

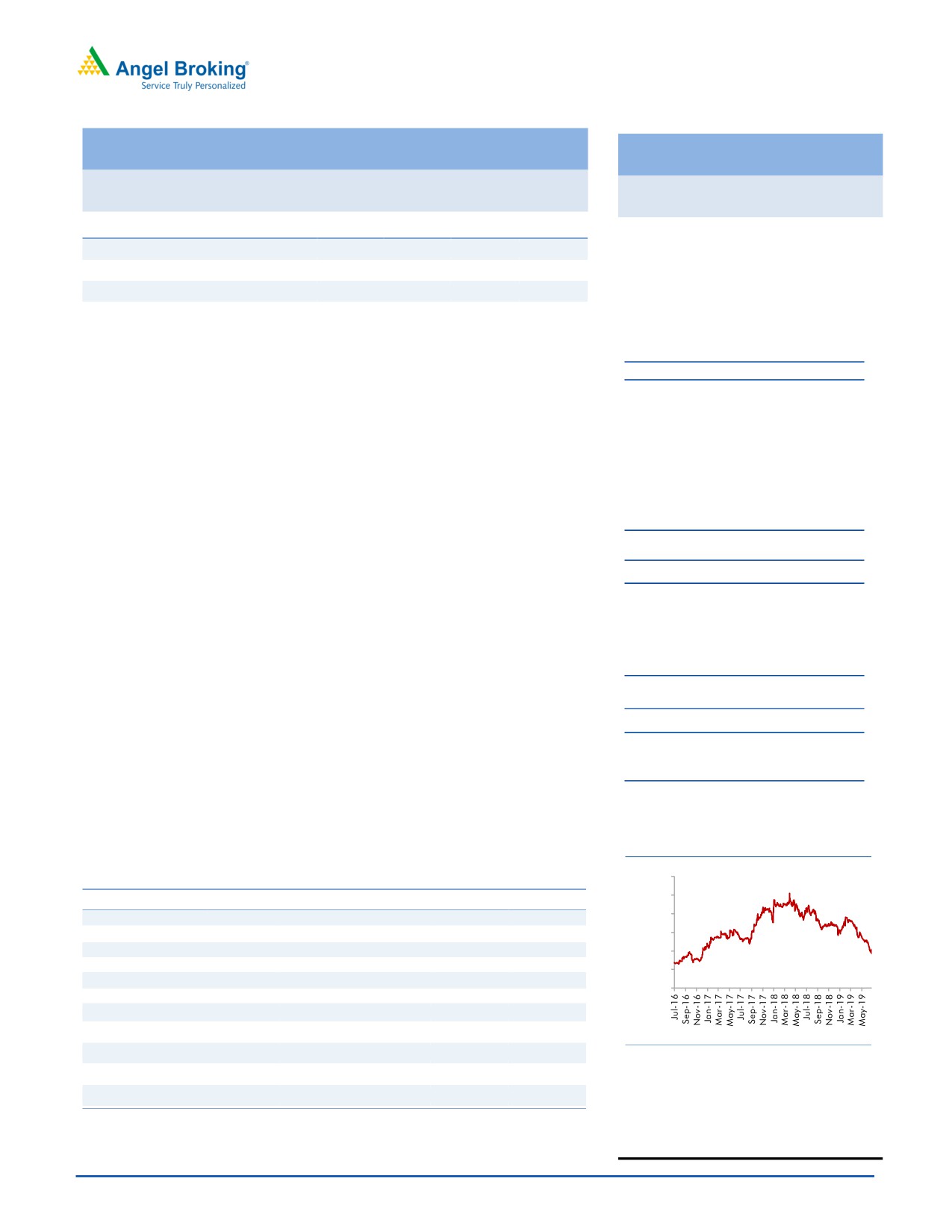

3 Years Performance charts

price of `1669.

3000

Key Financials

2500

Y/E March (` cr)

FY17

FY18

FY19

FY20E

FY21E

2000

Net Sales

1,271

1,650

1,851

1,822

1,968

1500

% chg

1

30

12

(2)

8

Net Profit

54

58

104

80

87

1000

% chg

4

7

79

(23)

8

500

EBITDA (%)

7.9%

8.2%

8.3%

9.1%

9.1%

0

EPS (Rs)

58

62

111

86

93

P/E (x)

22

21

12

15

14

P/BV (x)

3.9

3.3

2.8

2.4

2.1

RoE (%)

17.6

16.0

23.9

16.1

15.1

Source: Capitaline Angel Research

RoCE (%)

15.2

18.7

16.2

16.9

16.4

EV/EBITDA

12.7

9.6

8.5

7.8

7.2

Amarjeet S Maurya

022 39357600, Extn: 6831

Source: Company, Angel Research; Note: CMP as of august 09, 2019

August 09, 2019

1

LUMAX Industries | Q1FY20

Quarterly Financial Update

Y/E March (` cr)

1QFY20

1QFY19

% yoy

4QFY19

% qoq

FY2019

FY2018

% chg

Net Sales

402

482

(16.6)

433

(7.1)

1,851

1,649

12.3

Consumption of RM

239.8

310

(22.6)

273.5

(12.3)

1,183

971

21.8

(% of Sales)

59.6

64.3

63.2

63.9

58.9

Staff Costs

53

54

(1.2)

53

(0.5)

218.0

188.9

15.4

(% of Sales)

13.2

11.2

12.4

11.8

11.5

Other Expenses

71

78

(9.0)

75

(5.5)

297.7

355.6

(16.3)

(% of Sales)

17.6

16.2

17.3

16.1

21.6

Total Expenditure

364

441

(17.6)

402

(9.5)

1,698

1,516

12.1

Operating Profit

38

41

(5.5)

31

24.6

153

134

14.5

OPM

9.5

8.4

7.1

8.3

8.1

Interest

4.6

3.1

50.8

4.6

1.1

15.5

7.2

115.9

Depreciation

15.2

13.3

14.2

19.0

(19.9)

60.3

47.9

25.9

Other Income

4

4

11

56.9

18.9

PBT (excl. Ext Items)

23

28

(18.3)

18

22.7

134

98

37.7

Ext (Income)/Expense

PBT (incl. Ext Items)

23

28

(18.3)

18

22.7

134

98

37.7

(% of Sales)

5.6

5.8

4.3

7.3

5.9

Provision for Taxation

6

8

4

30.5

26.2

(% of PBT)

27.0

27.8

22.9

22.7

26.9

Reported PAT

17

20

(17.4)

14

16.2

104

71

45.5

PATM

4.1

4.2

3.3

5.6

4.3

Minority Interest After NP

Extra-ordinary Items

28

Reported PAT

17

20

(17.4)

14

16.2

75.8

71.4

6.3

Source: Company, Angel Research

August 09, 2019

2

LUMAX Industries | Q1FY20

Outlook and Valuation:

Near term outlook looks tough for the industry, however considering the long term

perspective, LIL is a good bet to play on auto growth and increasing LED penetration,

which will help Lumax to grow above the industry rate going forward. Thus, we main

our buy recommendation on the stock with target price of `1669.

Risks to our estimates

Slower than expected adoption of LED lights by OEMs and higher content of

impored raw material pose a downside risk to target revenue and net income

respectively.

Faster growth in PV and 2W segments pose an upside risk to target revenue.

August 09, 2019

3

LUMAX Industries | Q1FY20

Income statement

Y/E March (` cr)

FY18

FY19

FY20E

FY21E

Total operating income

1,650

1,851

1,822

1,968

% chg

30

12

(2)

8

Total Expenditure

1,515

1,698

1,657

1,789

Raw Material

1,104

1,183

1,152

1,240

Personnel

189

218

200

217

Selling and Administration Expenses

107

-

-

-

Others Expenses

115

298

304

333

EBITDA

135

153

165

179

% chg

33.9

13.4

7.9

8.4

(% of Net Sales)

8.2%

8.3%

9.1%

9.1%

Depreciation& Amortisation

48

60

63

68

EBIT

87

93

102

111

% chg

46

7

10

9

(% of Net Sales)

5

5

6

6

Interest & other Charges

8

16

18

20

Other Income

5

12

17

19

Extraordinary Items

-

36

Profit/Loss of Associate Company

13

9

9

9

Recurring PBT

98

134

110

119

% chg

51

38

(18)

8

Tax

26

30

30

32

PAT (reported)

71

104

80

87

% chg

31

45

(23)

8

(% of Net Sales)

4.3

5.6

4.4

4.4

Basic & Fully Diluted EPS (Rs)

62

111

86

93

% chg

7

79

(23)

8

Source: Company, Angel Research

August 09, 2019

4

LUMAX Industries | Q1FY20

Balance Sheet

Y/E March (`cr)

FY18

FY19

FY20E

FY21E

SOURCES OF FUNDS

Equity Share Capital

9.4

9.4

9.4

9.4

Reserves& Surplus

353

426

490

563

Shareholders Funds

362

435

499

573

Total Loans

101

138

102

102

Other Liabilities

47

42

42

42

Total Liabilities

510

615

643

717

APPLICATION OF FUNDS

Net Block

532

549

599

639

Capital Work-in-Progress

34

49

49

49

Investments

88

81

73

79

Long Term Loans & Advances

4

5

5

5

Current Assets

562

465

503

541

Inventories

169

204

225

243

Sundry Debtors

318

221

250

270

Cash

2

2

6

-2

Loans & Advances

1

1

1

2

Investments & Others

73

37

21

28

Current liabilities

721

574

602

627

Net Current Assets

-159

-109

-100

-87

Other Non Current Asset

11

40

24

48

Total Assets

510

615

643

717

Source: Company, Angel Research

Cash Flow

Y/E March (`cr)

FY18

FY19E

FY20E

FY21E

Profit before tax

98

134

110

119

Depreciation

48

60

63

68

Change in Working Capital

17

(132)

(115)

(50)

Interest / Dividend (Net)

8

16

18

20

Direct taxes paid

26

30

30

32

Others

(40)

(30)

(30)

(32)

Cash Flow from Operations

157

78

77

157

(Inc.)/ Dec. in Fixed Assets

(132)

9

(80)

(80)

(Inc.)/ Dec. in Investments

4

(4)

(7)

(18)

Cash Flow from Investing

(128)

5

(87)

(98)

Issue of Equity

-

-

-

-

Inc./(Dec.) in loans

19

36

-36

-

Others

(30)

(134)

49

(67)

Inc./(Dec.) in Cash

17

(15)

3

(8)

Opening Cash balances

1

19

4

6

Closing Cash balances

19

4

6

6

Source: Company, Angel Research

August 09, 2019

5

LUMAX Industries | Q1FY20

Key Ratio

Y/E March

FY18

FY19

FY20E FY21E

P/E (on FDEPS)

20.8

11.6

15.0

13.9

P/CEPS

11.3

7.3

8.4

7.8

P/BV

3.3

2.8

2.4

2.1

Dividend yield (%)

1.1

2.0

1.3

1.1

EV/Sales

0.8

0.7

0.7

0.7

EV/EBITDA

9.6

8.5

7.8

7.2

EV / Total Assets

2.3

2.3

2.3

1.7

Per Share Data (Rs)

EPS (Basic)

62.0

111.0

85.8

92.7

EPS (fully diluted)

62.0

111.0

85.8

92.7

Cash EPS

113.8

175.5

153.7

165.8

DPS

14.4

25.9

17.2

13.9

Book Value

387.2

465.1

533.8

612.6

Returns (%)

ROCE

16.0

23.9

16.1

15.1

Angel ROIC (Pre-tax)

18.7

16.2

16.9

16.4

ROE

22.4

19.2

19.7

18.8

Turnover ratios (x)

Inventory / Sales (days)

37

40

45

45

Receivables (days)

70

44

50

50

Payables (days)

119

75

70

70

Working capital cycle (ex-cash) (days)

(11)

9

25

25

Source: Company, Angel Research

August 09, 2019

6

LUMAX Industries | Q1FY20

Research Team Tel: 022 - 39357800

DISCLAIMER:

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited, Bombay Stock

Exchange Limited, Metropolitan Stock Exchange Limited, Multi Commodity Exchange of India Ltd and National Commodity & Derivatives Exchange

Ltd It is also registered as a Depository Participant with CDSL and Portfolio Manager and Investment Adviser with SEBI. It also has registration

with AMFI as a Mutual Fund Distributor. Angel Broking Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research

Analyst) Regulations, 2014 vide registration number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any

other regulatory authority for accessing /dealing in securities Market. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision.

Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations

as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document

(including the merits and risks involved), and should consult their own advisors to determine the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading

volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals. Investors

are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed

to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general guidance

only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise

to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has not independently verified all the

information contained within this document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the

accuracy, contents or data contained within this document. While Angel Broking Limited endeavors to update on a reasonable basis the

information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or

passed on, directly or indirectly.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection

with the use of this information.

Disclosure of Interest Statement

Lumax Industries

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

August 09, 2019

7